The SWIFT Exodus: How Digital Payments Are Revolutionizing Treasury Operations

SWIFT, though impressive in scale, is showing its age in this rapidly evolving landscape.

Introduction: The Backbone That’s Showing Its Age

I still remember my early days interning at Deloitte, seeing global enterprises trying to streamline their cross-border financial operations. SWIFT was the undisputed titan, the backbone that connected financial institutions across the globe. With over 11,000 member institutions spanning more than 200 countries, SWIFT’s dominance seemed untouchable. However, fast forward to today, and the world of global payments looks dramatically different. Digital payments have surged, and the era of instant, transparent, and affordable global payouts has begun. SWIFT, though impressive in scale, is showing its age in this rapidly evolving landscape.

What is SWIFT, Exactly?

SWIFT, or the Society for Worldwide Interbank Financial Telecommunication, is essentially a global messaging network used by banks and financial institutions to quickly, accurately, and securely send and receive information, such as money transfer instructions. It doesn’t transfer money itself but enables banks to communicate securely and reliably. However, SWIFT operates on a messaging system from the 1970s, significantly limiting its ability to adapt swiftly to the demands of modern, instant financial transactions. This fundamental technological limitation makes its eventual downfall inevitable in the face of rapid payment innovation.

SWIFT’s Key Problems

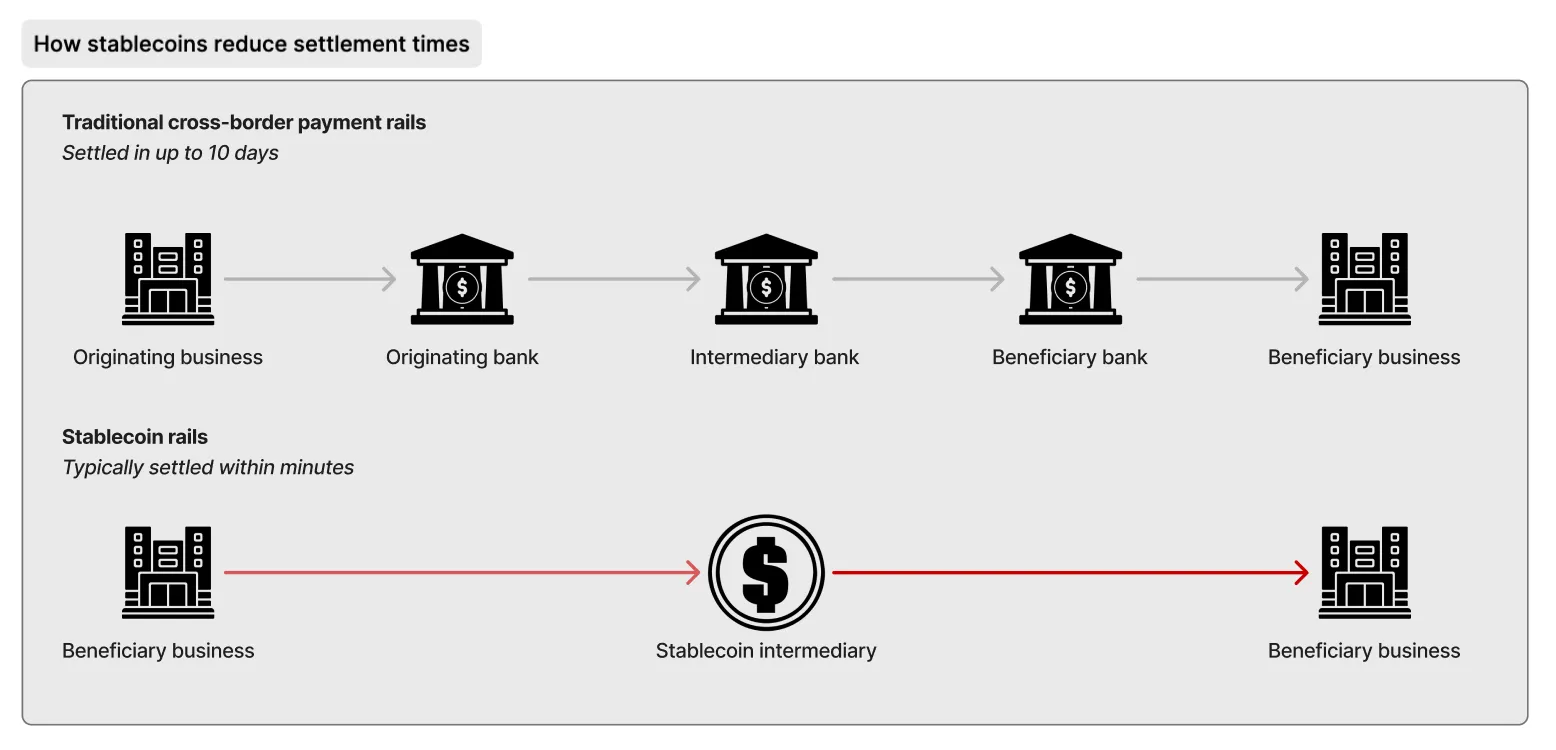

Slow Settlement Times

Typical SWIFT transactions take anywhere from 1 to 5 business days. This sluggish pace results from SWIFT’s correspondent banking system, a complex multi-step process involving intermediaries. For businesses needing real-time transactions—think logistics companies paying international suppliers—these delays are significant roadblocks.

High Costs and Opaque Fees

Sending money internationally via SWIFT typically costs between $30–$50 per transfer, often accompanied by hidden fees and unpredictable FX markups [source: World Bank Remittance Prices]. This lack of transparency is problematic for treasury teams managing budgets and freelancers receiving cross-border wages.

Lack of Transparency

The absence of real-time tracking capabilities means treasury teams often find themselves in limbo, uncertain of a payment’s location or status. Resolving lost or stalled payments can take days or even weeks, severely impacting cash flow and supplier relationships.

Exclusion and Limited Access

SWIFT caters exclusively to fully banked institutions, inadvertently excluding billions in emerging markets. The consequences disproportionately affect freelancers, gig workers, and consumers in regions such as Asia, Africa, and Latin America.

Outdated Technology & Security Risks

Originating from the 1970s, SWIFT’s technology remains messaging-based, facilitating communications but not directly transferring money. The infamous Bangladesh Bank hack in 2016, resulting in an $81 million loss, starkly exposed the vulnerabilities of this outdated system.

Real-World Consequences

The inefficiencies inherent in SWIFT manifest acutely in various sectors:

- Businesses: Delays lead to cash-flow disruptions, lost opportunities, and strained supplier relationships.

- Freelancers/Gig Workers: Professionals in Asia, Africa, and Latin America frequently face prolonged delays or even lost wages, severely impacting their livelihoods.

- Consumers: Migrants and families relying on remittances bear excessively high costs, with fees significantly reducing the money received.

Why Now? The Opportunity for Change

We stand at a transformative moment for payment innovation. Blockchain payments, stablecoins, and modern digital rails provide what SWIFT cannot: instant settlement, total transparency, global accessibility, and enhanced security through programmable money.

In my experience working at the crossroads of fintech and treasury, I’ve seen firsthand how these emerging technologies radically improve global payouts. Companies adopting these new payment solutions report fewer delays, greater transparency, and substantial cost savings.

The Promised Land: What a Better System Looks Like

Imagine a future where cross-border payments move as effortlessly and instantaneously as emails. A world where anyone, irrespective of their banking status, can securely send and receive money. This ideal system is transparent, auditable, secure, and immune to censorship and geopolitical whims.

Blockchain payments and stablecoins already offer this promise. These technologies make financial inclusion a reality, providing global access without the exorbitant fees and uncertainties of traditional methods.

Call to Action

It’s time for treasury leaders, CFOs, and finance innovators to critically assess their dependence on SWIFT. We challenge our industry peers: Audit your current payment processes, analyze costs, and actively pursue digital transformation. Embrace next-gen payment solutions and position your treasury team at the forefront of this inevitable payment revolution.

FAQs

1. What are alternatives to SWIFT for international treasury operations?

Blockchain-based payment solutions, stablecoins, RippleNet, and direct fintech payment rails.

2. How do blockchain payments improve cross-border transactions?

Blockchain transactions offer instant settlement, transparency, lower costs, and improved security.

3. Are blockchain payments secure for large treasury transactions?

Yes, blockchain payments use cryptographic security, providing high security and transparency for large transactions.

4. Why are stablecoins gaining popularity in global payouts?

Stablecoins offer stability against volatility, fast transaction times, lower fees, and improved financial inclusion.

5. Can blockchain payments replace SWIFT entirely?

While blockchain solutions can significantly enhance cross-border payments, complete replacement may be gradual as legacy systems coexist during the transition period.

6. What impact do digital payments have on unbanked populations?

Digital payments facilitate financial inclusion by providing access to global financial services without traditional bank accounts.

7. How can international treasury teams start integrating blockchain solutions?

Begin with pilot programs, partner with reputable fintech providers, and gradually scale up to fully integrated blockchain solutions.